The hardest part of setting a budget is getting started. After all, it’s a task that comes with a lot of baggage. Sure, sweeping the floor or making the bed might not be enjoyable. Still, at least it’s not likely to send you into an existential spiral that makes you question your past, present, and future, as well as your self-worth, the meaning of life, why the sky is blue, why the world is round, et cetera.

Budgeting tips for beginners that you’ll actually want to follow

- Written by

-

![A headshot of Rachel Cribby who is a contributing author at WealthRocket]()

- Edited by

-

Why you can trust us

The team at WealthRocket only recommends products and services that we would use ourselves and that we believe will provide value to our readers. However, we advocate for you to continue to do your own research and make educated decisions.

Okay — even if you find that forcing yourself to think about money doesn’t send you into that very specific lament, everyone can use some unique budgeting tips now and then to achieve a bit of harmony in their financial life.

This article will provide accessible and creative budgeting ideas that can help you cut down on stress and achieve your financial goals, whatever they may be.

1. An emergency fund is your foundation

Would this really be an article about budgeting tips if we didn’t get the first harp on an emergency fund’s importance, at least for a little while?

Before you even start creating a budget for yourself, and especially before you even start thinking about your long-term goals, it’s a good idea to determine what a comfortable emergency fund looks like for you.

For some individuals, $1,000 may be enough to have them feel comfortable. Others won’t sleep well at night without at least three months worth of expenses set aside. There is no magic formula to determine how much money you should stash aside in your emergency fund. Instead, it’s a personal choice.

If you do not yet have an emergency fund established, it may be in your best interest to allocate a certain amount of your take-home income to save up for one.

Once you’ve established an emergency fund savings account, you can start saving money for other goals (preferably of the fun variety).

2. Have a savings plan that works for you — not for somebody else

Your friends may try to offer you financial advice — and many of us would be lying if we said we have never offered financial advice to our friends — but unless they are a professional accountant that knows the intricacies of your financial situation, chances are that they cannot accurately tell you how to spend or save money.

3. Don’t feel obligated to track your spending (but do spend money mindfully)

Take a deep breath. You have already made it a decent distance into reading this article, which means that you are taking proactive steps towards building an effective budget and setting financial goals for yourself.

4. Work out a debt repayment schedule that inspires you

If you are grappling with debt, you are not alone. In fact, an estimated 73.2% of Canadian adults and 80% of American adults are carrying at least some outstanding balances, whether it be in the form of credit card debt or student loans.

5. Start saving for retirement early — even if it’s a small amount

Wealthsimple

- Account Fees 0.4%-0.5%

- Minimum Deposit $1

- Asset Types Bonds (government and corporate), Real Estate, ETFs, Gold, Mutual Funds, and Currencies

Rachel Cribby

Frequently Asked Questions

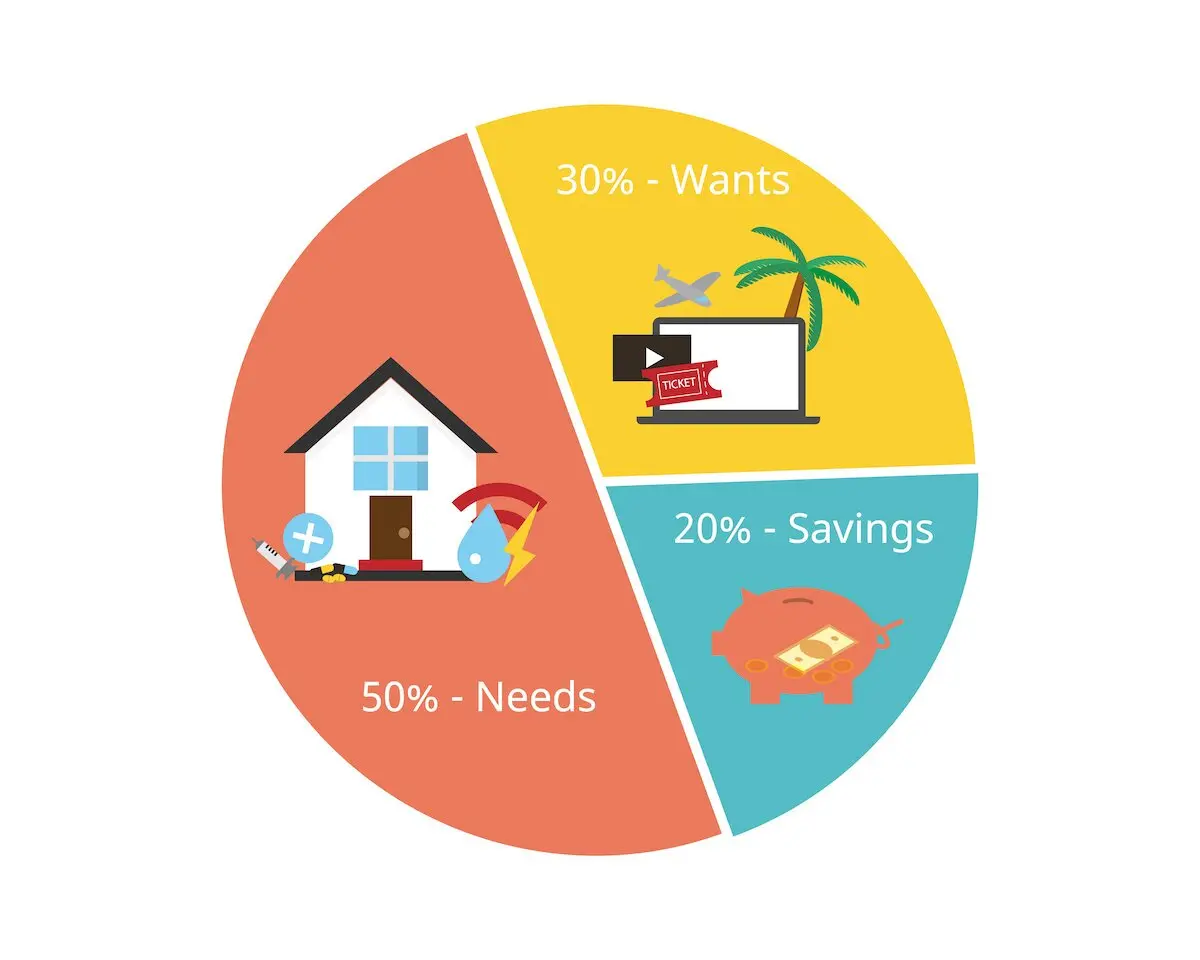

The answer to this question is personal! Instead of dollar amounts, let’s answer with a percentage. According to the popular budgeting philosophy of the 50/30/20 rule, 20% of your income should be spent on savings and debt. So, depending on the amount of debt you have, you should be putting up to 20% of your income towards your saving goals.

We’re glad you asked! In today’s technologically-driven age, it makes sense that “there’s an app for that”. Check out our review of the best budgeting apps.