When you’re engrossed in the process of budgeting, the last thing that you want to do is think about even more numbers. After all, there is nothing like a day of crunching digits to make our heads dizzy.

What is The 50/30/20 Rule?

- Written by

-

![A headshot of Rachel Cribby who is a contributing author at WealthRocket]()

- Edited by

-

Why you can trust us

The team at WealthRocket only recommends products and services that we would use ourselves and that we believe will provide value to our readers. However, we advocate for you to continue to do your own research and make educated decisions.

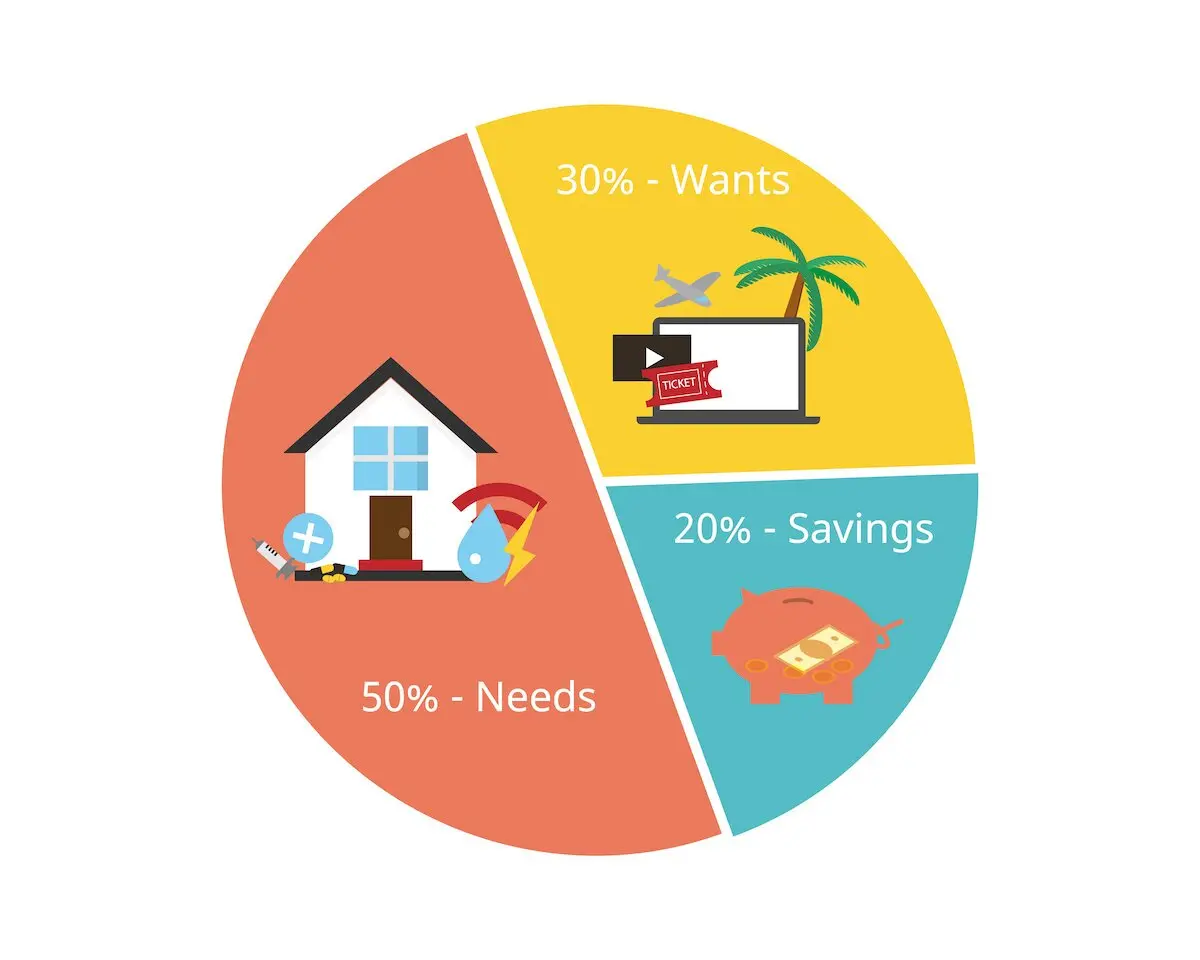

What is the 50/30/20 rule?

How does the 50/30/20 rule work?

If this budget looks good to you on paper, you may be wondering how to apply it to your life.

Thankfully, the 50/30/20 is as easy to implement as it is to understand. What’s better is that when implemented correctly, the 50/30/20 can help you save money, pay off debt, and have fun.

Here are some simple steps to help you use the 50/30/20 budget towards your unique financial goals:

- Take a look at your income: It’s important to note down not what your pre-tax income is but your post-tax (i.e. take-home) income.

- Make a note of your immediate needs: ensuring that they add up to 50% of your income. If you find yourself overspending, it might be a good opportunity to look at the areas in your life that you can cut back on, if possible. You may have to compensate by cutting back on your income’s next portion, which means your wants.

- Make a list of all of your wants: Try limiting yourself to a total of 30% of your overall budget.

- Make a list of your long term saving goals: 20% of your budget will be designated for this, whether it be putting money into a savings account with a high-interest rate or putting money into a retirement account.

- Hold yourself accountable!: It’s okay if sticking to your budget feels harder on some months than others, but consistency is also important.

EQ Bank

- Account Options Hybrid Savings/Chequing, Investment Accounts

- Countries Served Canada Only

- Branches in Canada Online only

- Savings accounts offered

- Savings Plus Account

- Joint Savings Plus Account

- TFSA

- RSP

- FHSA

- U.S. Dollar Account

- Reloadable EQ Bank Card

- Registered and non-registered GICs

- Send international money transfers with Wise

- Fixed and variable mortgages

- No monthly fees

- Free bill payments

- Free EQ to EQ transfers

Pros & cons of the 50/30/20 rule

Pros

Flexibility works well for fluctuating income

Allocating 20% of your budget to saving can help with long term goals

Can effectively pay down debt quickly

Cons

Impractical for those on very strict incomes who may not have as much room for “wants”

May not be the best option for those who are looking to pay down high-interest debt as quickly as possible

Rachel Cribby

Frequently asked questions

As a matter of fact, yes. Senator Elizabeth Warren coined this budget’s term and created the concept in her 2006 book “All Your Worth: the Ultimate Lifetime Money Plan”.

It certainly holds that potential. If you are able to stick to a 50/30/20 budget, 20% is a considerable amount of your income to put towards savings. It will, of course, depend on the amount of debt you carry as well as the nature of your post-tax income.